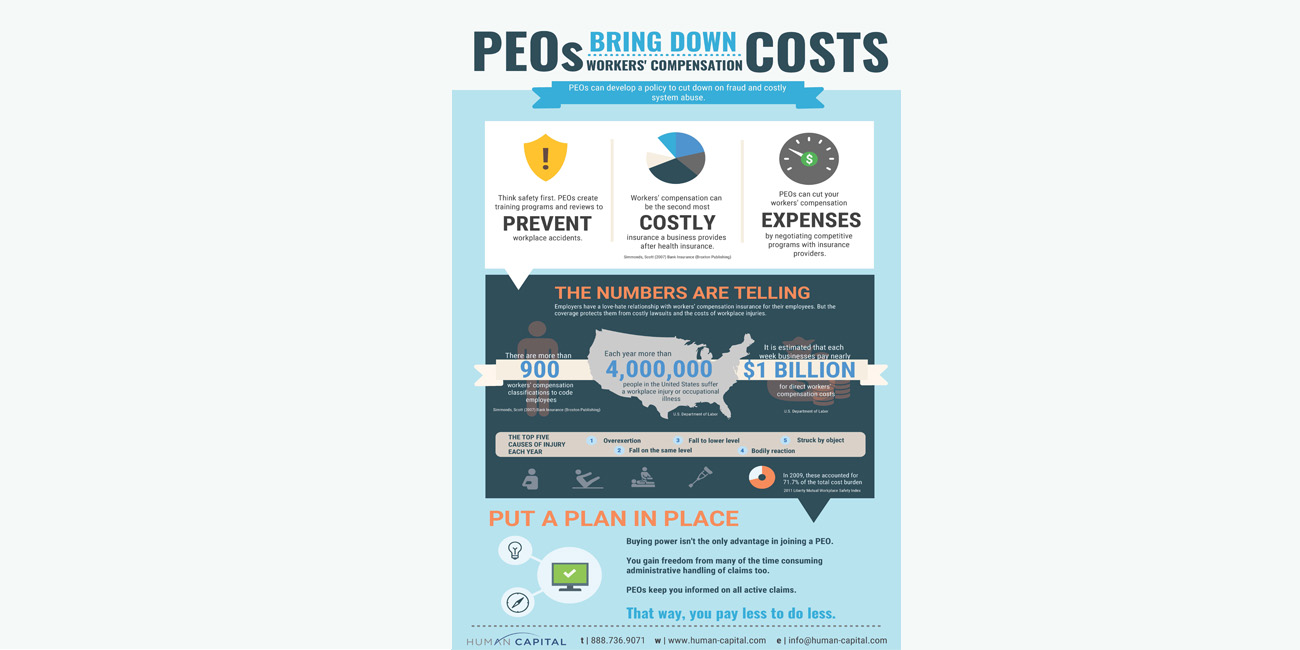

Many, if not all, companies are at risk for workers’ compensation incidents and should be informed of state and federal regulations and legislation, establish clear policies and procedures for such claims, and stay proactive in preventative methods. There are countless ways to address and prevent workers’ compensation issues, but here are the basics all business owners and employers should know.

How to File a Claim[1]

Generally, in filing a workers’ compensation claim, there are two parts of the process: the employer’s role and the employee’s role.

The employer must:

- Provide the employee with the appropriate paperwork and guidance

- File the claim with the insurer

- Comply with state law for reporting the work injury

The employee must:

- Notify the employer of the injury, including:

- the date, time, and location of injury;

- type of injury (i.e., affected areas of the body);

- parties involved in the accident (if any);

- how it occurred; and

- medical treatment received.

- File a formal workers’ compensation claim.

*NOTE: It is important for the employee to understand what types of injuries/claims are not typically accepted.

- Stress or psychiatric injuries

- Self-inflicted injuries

- Injuries caused by misconduct (i.e., fighting, goofing around)

- Injuries obtained while commuting to or from work

- Injuries incurred while violating company policies (i.e., under the influence, committing a crime)

Once the claim is filed, no further action is typically required. It is strongly recommended that the injured employee keep detailed records of any follow ups made on the claims, as well as how the injury affects work and day-to-day activities and all receipts for any expenses that were the result of the injury. These records will aid if your claim is rejected and you have the opportunity to appeal. Workers’ compensation claims vary from state to state. It is best to familiarize yourself with your state’s policies and regulations for workers’ comp claims.

If you need help with enacting more effective workers’ compensation policies or would like to evaluate other options available in the market, please contact Human Capital. We have a team of workers’ compensation, compliance, and risk management professionals who can assist with finding the best solution for your business needs.

[1] https://www.insureon.com/small-business-insurance/workers-compensation/how-to-file-a-claim